Category: Uncategorised

I hope you are keeping well, and as I am writing this the temperature outside is 34 degrees so I trust that you are managing to enjoy the weather (although being British, I do feel this is a bit too hot!).

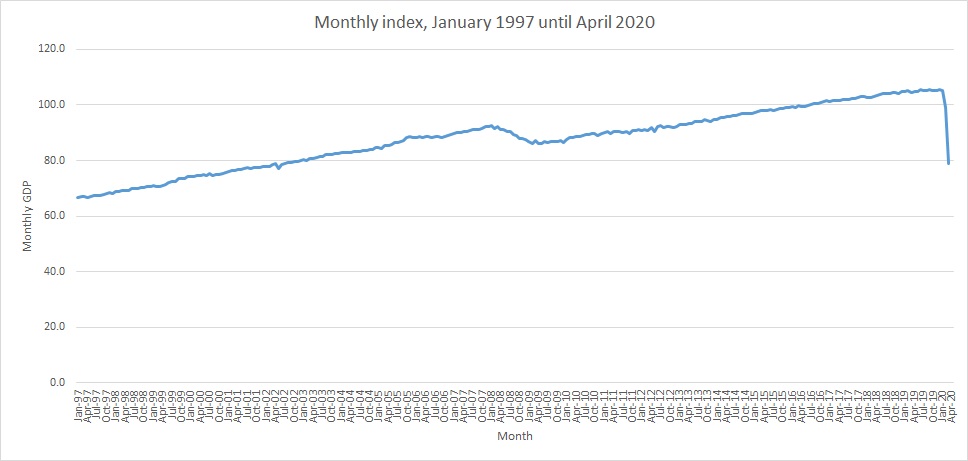

As I predicted in my previous update, the latest GDP figures for the UK have officially shown that we have entered a recession. As predictions go, it wasn’t a particularly bold one, and I think that we all knew this was coming.

To put into context, GDP shrunk by 20.4% in the second quarter, which was broadly in line with the market expectations. Previously, GDP fell by 2.2% in the first quarter. However, lockdown was only announced on 23 March in the UK, so the effect of the pandemic was largely seen in the following quarter.

Nevertheless, this is the biggest GDP quarter drop on record, and is the first time the UK has been in recession for 11 years. However, amongst these very gloomy figures, it should be noted that GDP grew by 1.8% in May, and by a further 8.7% in June.

In addition, with the news of the UK falling into recession and a record quarterly drop, you would have expected the FTSE100 to have fallen in a similar manner. However, you would be mistaken. On the same day that the recession was announced, the FTSE100 actually grew by a very healthy 2.04%.

However, here lies the issues with investment markets compared with economic data and news. If you read the papers, listen to the news or read social media, they tend to very much reflect the economic news, which at the moment is not positive. And that is not necessarily wrong, as being in a recession can affect many aspects of our day-to-day lives.

However, share prices tend to be more a reflection of the future, rather than the present. Official economic data, is of course, in its nature, a record of the recent past. The investment markets already knew this had happened, and as mentioned, the GDP figures were very much in line with their expectations. The FTSE100 rose sharply on the day of the announcements as it sees tiny shoots of the economy beginning to recover, and is hopeful these will continue.

Another example of how the investment markets tend to be ahead of the economic data was seen at the beginning of the pandemic. From the end of February, the global investment markets plummeted as the virus outbreak became a global pandemic. At this point, the official economic data would not have reflected this at all, but the investment markets accurately predicted the impact this was about to have on the global economies.

Having said all this, to reiterate a point in my last update, I still feel the markets are in a ‘wait and see’ period. We are seeing an increase of cases across Europe, and there will be nervousness to see if these develop into second waves. Unexpected good news, such as a proven vaccine, or unexpected bad news, such as second waves, can see relatively volatile movements in the investment markets.

As always, if you would like more information or advice about your investments or any other matter in regards to the markets and the latest economic data, please do get in touch.

Enjoy the rest of the summer, and I hope the warm weather holds (albeit a little cooler for me please!).

Richard Brazier – Director – Hanover Financial Management Limited

|

|

I hope you are all keeping well as we come out of lockdown - fingers crossed the government are correct in their hope that we will see a return to normal by the end of the year.

In this month’s update, I thought I would look into the future and predict the investment outlook for the next few months. To recap, we saw the global markets fall dramatically through March as the pandemic really took hold around the world. As we have seen in the UK and internationally, governments and central banks have been very quick to act in an attempt to ease the impact Covid-19 has had on the global economies. This has had a positive effect on the markets which have recovered some of the losses that they saw during March. However, I think we have now entered a ‘wait and see’ period. There is much uncertainty and nervousness around potential second waves; whether the stimulus packages will work; and indeed, the increasing number of cases in the US.

One thing we can say with some certainty is that we are about to enter a recession. However, the length and severity of this recession is unknown, as the economic repercussions are still to be fully understood. As lockdown measures are eased, the UK government will be hoping the reopening of the economy will see a quick recovery. Nevertheless, recent figures illustrate an eye-watering drop in GDP, and I think it will take some time to recover, and certainly won’t rise as quickly as it has fallen.

With the various stimulus packages that are being introduced, this is leading to the largest rise in government debt levels we’ve seen since World War II. At some point, how this debt will be repaid will need to be addressed, but that is very much an action for the future.

In addition to global pandemic, the US Presidential election is also on the horizon. As mentioned in a previous blog, prior to the pandemic, I thought that President Trump would have based his campaign on how well he had managed the economy. For this reason, he will require a swift recovery and further gains in the US stock market in the coming months. This is probably why he has been so keen to reopen the US economy - perhaps earlier than it should have.

I believe the markets could be best described as being pessimistic at the moment as they wait to see how the next few months unfold. For this reason, there could still be short-term volatility as good or bad news is reported. I certainly don’t think the economy will return to its original position as quickly as the down turn took effect.

As always, for more information and advice regarding your investments, please do not hesitate to get in contact with us. Hopefully, it won’t be much longer before we can resume as ‘normal’ and see you again.

|

Richard Brazier – Director – Hanover Financial Management Limited

|

|

After entering the lockdown at the end of March, the overriding sense I get from most people is that they are now bored, and looking forward to a return to normal life. Thankfully, the lockdown measures are being eased, albeit at different rates throughout the UK. I was thankful that I was able to take the children over to see their grandparents for the first time in months a few days ago.

I have my fingers crossed that there won’t be a second wave, which will dent our own personal morale and no doubt the investment markets as well. Thankfully, as we have seen the lockdowns eased around the world a second wave doesn’t appear to have materialised at this time.

In fact, very heartening, the investment markets have continued to rebound from the low point seen in March, when the lockdowns were in force around the world. All the major indices saw positive returns through May, and this has been reflected in your investment portfolios. We are still a way away from the valuations seen at the beginning of February, but hopefully it is a source for optimism.

It never ceases to amaze me how the investment markets at times can seem oblivious to the economic data that is being seen, yet continue to produce positive returns. Of course, the reality is that they aren’t ignoring this data, more that this has already been priced into the markets. What adversely affects the global markets, in either direction, is surprising news. An example of this was seen recently when the expert consensus was that the US was going to see unemployment figures pushing 20%. The actual released figures actually showed that there had been a decline, which saw markets around the world increase on this news.

Having said all this, the economic figures that are being released, still take some comprehension as they show the effect this pandemic has had. For instance, the UK saw a drop of over 20% GDP in April.

Let’s hope that as the lockdown is lifted businesses can start to return to some degree of normal. Although I do think it will take some time and wonder what the ‘new normal’ will look like for all of us.

Although the global markets have been showing an upturn over the last two months, I still believe it is far too soon to say that we are over the worst. There is still a lot of volatility, and the true cost of this pandemic is yet to be seen. However, we will look to keep you as updated as we can on your investment portfolios during this time. As you know our view is that investment strategies should be for the long term, and that remains the case.

We are all available to speak to you, whether that is to discuss your investments or simply to catch up. Like you, we are all looking forward to being able to get out more, and to see you all in person.

|

Richard Brazier – Director – Hanover Financial Management Limited

|

|

I trust that you are all keeping well in these challenging times, and like me, are looking forward to a return to the ‘new normal’ soon.

I wanted to start this monthly update with some positive news; something that I think has been sorely lacking in the last few weeks. After the historic drop across the global financial markets from mid-February to the end of March, we saw an upturn from these same markets in April. One of my bug bears is that mainstream media only provide the negative news in relation to investment markets. Therefore, whilst news outlets were letting people know how badly the markets were performing during this period, they were much quieter during April when the markets began to improve.

Statistically speaking, the FTSE 100 fell to a low closing price of 4,993.89 on 23 March 2020, but by 30 April 2020 the closing price had risen to 5,901.21, and even passed 6,000.00 the day before. This meant the index had increased by over 18% in this time period.

Throughout the same period, the Dow Jones Industrial Average (a stock market index that measures the performance of 30 large companies listed on stock exchanges in the United States) increased by over 19%.

As a result, these increases were reflected, to a degree, in your own investment portfolios throughout April. Of course, as you will be aware, your portfolio will not be wholly invested in these stock markets, but depending on your risk profile, will have exposure to varying degrees in the global markets.

Despite the increases that were seen during last month, there was still far more volatility than normal. During the last few years, seeing a 2% increase or decrease within a day was a rare occurrence. However, over the last few weeks, this has been very common. The impact of Covid-19 is still causing financial uncertainty, and as a result, it is in my opinion still far too early to suggest the worst is behind us. However, the positive returns throughout April has to be welcomed with open arms.

Another area that is likely to cause more uncertainty in the performance of your investment portfolios will be the increasing tension between the US and China. Before the current crisis, there had been some easing of the tension between the two over their ongoing trade war. However, in the last week or so, the Trump administration have been more and more vocal in their claims as to where the Coronavirus originated; coupled with President Trump sending numerous anti-China tweets.

This, along with some negative economic news at the end of April, has seen some negative sentiment return to the markets. As this is an election year in the US, and I think it is safe to say that President Trump would have pinned a lot of his campaign on his success in creating jobs and market performance, he will be looking to blame China for this current crisis. If this conflict continues, I predict this will impact global market recoveries.

To finish on a positive note, I believe that finding a treatment and/or vaccine for the virus would probably outweigh the negatives of a second trade war between the US and China, at least in the short term.

We are still open for business, so if you have any queries or concerns at this time, get in touch with one of our financial advisers today.

Stay safe and we look forward to seeing you again soon.

|

Richard Brazier – Director – Hanover Financial Management Limited

|

|

As the global COVID-19 pandemic progresses, you may have queries and concerns about the performance of your investments. Specifically, our clients have seen a significant decrease in the value of their portfolios within a short space of time. We are here - to ask you not to panic, and to reassure you that during these difficult times, we are still open for business. For more information and advice, call one of our financial advisers today.

We recognise your questions and concerns - as we are all in the same boat. In my own experience, my lockdown has been very much bitter sweet to date. My son had a last minute dash back from university when he finally realised the government were locking down the country, and as mentioned in my previous blog article, my daughter was due to be sitting her GCSEs this summer, which of course, are now not going ahead. She has still been doing school work, whilst learning how her grades will be assessed in the summer.

It has however, been good to spend so much time with my family during this period - even if the shopping bill has somewhat increased!

On the bitter side, the lockdown has meant I haven’t been able to see my fiancée, who lives with her daughter in another town to myself. This has been incredibly difficult, although I am thankful for the wonders of modern technology which have enabled us to keep in contact via Facetime.

Of course, I realise that many people are having to deal with issues far more difficult than mine - and I am thankful that all my family and friends are all currently safe and well.

I have found this time to be quite reflective, a chance to assess all aspects of my life. For instance, I have been in touch with people close to me far more than I normally would have, and hope that this continues once the lockdown is over.

I, like many of our clients, have found that I have time to plan for my future; by making sure my Will, life cover and other financial aspects of my affairs are in place and up to date. If you need guidance whilst planning your financial affairs, we can place your individual concerns in the trustworthy hands of our legal experts at Ince.

Finally, during this enforced lockdown I have noticed that there seems to be some pressures to learn something new, like an instrument or a foreign language. In my opinion - do what it takes to get your through this period of time. If that is sitting in front of the TV, watching films or a new series on Netflix - so be it (no guesses for what I have been doing!).

|

Richard Brazier – Director – Hanover Financial Management Limited

|

|

Firstly and most importantly, I hope you are staying fit and healthy whilst managing to cope with the current circumstances and Government measures. These are certainly unprecedented times, and I can only keep my fingers crossed that life will return to normal soon.

In regards to investment portfolios, you will have no doubt seen how the global investment markets have fallen especially since the outbreak took hold in Italy, and subsequently the rest of Europe. Much of the fall was initially through fear and uncertainty, followed by concerns on how much damage this will do to the world’s economies in the longer term.

Governments and Central Banks have been very quick to announce a multitude of financial measures and stimuli but these have done little to alleviate the fears of the global markets. However, on the back of the latest stimulus plans that were agreed in the US, the markets rose for three days running at the end of last week. Showing how volatile the markets have been this hasn’t happened since February.

I would not like to say this will be the end of any falls, or that the bottom has been reached, as we are in unchartered territory. Indeed, already this week we have seen sharp increases and decreases in the markets and I suspect the volatility will continue for some time to come.

It is an easy thing to say, but I realise from my own investment portfolio not an easy thing to practice, which is not to panic at this time. History has always shown that shares have a good record of generating real returns over the long term, and these falls eventually become blips on performance graphs. It is also true to say that bear markets (where a market falls by 20%), such as the one we have now entered, have always been far shorter than bull markets (where a market is on the rise).

I realise this is a very unsettling period, as we all come to terms with the Government lockdown. I am having to get used to home schooling my daughter who was meant to be sitting her GCSE exams this summer! At Hanover we are all getting used to working remotely, as per the Government guidelines, which I do not envisage impacting on our service capabilities to you.

For more information and support, please do not hesitate to contact your adviser. In the meantime please stay safe and we look forward to seeing you soon.

Richard Brazier – Director – Hanover Financial Management Limited

To help employers through current difficult times, the Government has introduced the Coronavirus Job Retention Scheme. The aim is for employers to “Furlough” employees rather than lay off staff, with the Government paying some of the costs.

Coronavirus Job Retention Scheme

The main features of the Scheme are as follows:-

- In force for at least 3 months, starting 1 March 2020.

- Claim 80% of furloughed employee’s salary, up to £2,500 a month.

- Covers employers NI contributions and minimum Automatic Enrolment Contributions (i.e. 3% of salary above Lower Earnings Limit, which is £512 a month for March and £520 a month from 6 April 2020).

- The employee’s salary is subject to the normal deductions for tax, NI and Pension.

- For an employee on Statutory Sick Pay - they can be furloughed once this ends.

- An employee who is on Statutory Maternity Pay remains eligible for 90% of average weekly earnings for the first 6 weeks and lower of 90% of average weekly earnings or SMP at £148.68 per week up to 5 April 2020 and £151.20 from 6 April 2020. If employer offers enhanced pay during maternity, the additional payments are “wage costs” and are covered by the Scheme.

- The online system to claim will be available at the end of April 2020.

Pension Contributions

For furloughed employees the following applies:-

- Salaries under the scheme are pensionable so employees will need to pay pension contributions (unless they elect to opt out).

- If employer tops up the pay then the employee must pay pension contributions on the actual salary paid.

- Employers will receive support for employee contributions at the minimum AE required level, (with a band of excluded earnings) so if their scheme is more generous then they will need to pay the additional employer contributions.

- Employers still have all their obligations under both Automatic Enrolment legislation and their contractual commitments to staff (which they may seek to vary, but may need to take legal advice on the impact of this).

The Pensions Regulator (TPR)

The requirement to continue with Automatic Enrolment contributions has not been lifted, as some had hoped. However, the following should be noted:-

- TPR have indicated that they will give employers more time to pay their automatic enrolment contributions before using their enforcement powers.

- TPR are not suspending all enforcement activity, as employers still have a duty to pay pension contributions in a timely manner.

- Pension providers have been asked to be flexible when agreeing payment plans.

- In the longer term, all missed contributions must be made up in full, so that staff do not miss out.

Other Benefits

As a furloughed employee remains an employee on contract, all their normal benefits continue to apply. The precise details of how this works in practice are still being considered. However:-

- Group Life insurers have indicated that claims are likely to be paid based on pre furloughed salary.

- Group Income protection insurers have also indicated that claims are likely to be based on pre furloughed salary, but are considering the position as in some cases this could lead to the insured benefit being higher than the reduced furlough pay. With the issue of self-isolation they are also considering how the start of the deferred period should be determined.

- Group medical insurers have typically adjusted some of their benefits. For example, in some cases increasing the NHS cash benefit if admission is due to Covid 19, and funding video or telephone consultations with medical consultants. As the Government takes over much of the private hospital network and staff to assist in dealing with the crisis, private hospitals are starting to cancel non-emergency operations. For conditions already approved, typically if the procedure is cancelled, the approval can be carried forward. Physiotherapy sessions have largely moved online and insurers are seeing increased demand for video and telephone GP support and for online and telephone counselling services to assist with mental health and other issues.

- The coronavirus itself is not a critical illness covered by Group Critical Illness policies. However, if the virus leads onto a condition that is covered then insurers are considering claims.

- With schools and nurseries shut and many working from home, many employees are reducing their orders for Childcare vouchers. As this scheme is now closed to new entrants, employees should be reminded that if they take a break of more than 12 months then (under current rules) they will not be able to start again.

Comments

All of the above should provide some help to businesses in these difficult and challenging times. Claims under the Job Retention Scheme cannot be made until the portal is up and running which will not be until end of April. In the meantime, businesses are encouraged to apply for Coronavirus business interruption loans, from the British Business Bank, if they need funding support before it is possible to apply for the grants under the Job Retention Scheme.

All current employment legislation remains in place and as a reduction in salary is a contract variation, employers should generally seek the consent of employees to changes and seek legal advice to clarify the impacts and risks of any changes as necessary.

It is good to see that the Pensions Regulator is prepared to be flexible, but note that this is just on timing of the payments as ultimately all amounts due must be paid. The impact of investment return on member funds does not appear to have been considered currently, but if investment markets have risen significantly by the time payments are caught up there is a potential issue of claims for missed investment return.

It is important to remember that a furloughed employee remains an employee and entitled to all their normal employee benefits. As we move forward through this difficult time the position on how this will impact all benefits will hopefully become clearer, as insurers have time to consider the position but at the moment this is a fast moving landscape.

How we can help

If you would like to discuss any aspect of this article please don't hesitate to contact Robert Young or Graham Smithson.

Clients frequently ask us this question and this article is designed to give you a basic overview of the legislation governing pension fund death benefits. However, nothing is an adequate substitute for specific information tailored to your personal circumstances, so if you would like further information please get in touch with us for more specific guidance.

Pension fund death benefits

The answer to this question will depend on not only legislation, but also the rules of your pension fund. Therefore, your first step should be to consult your pension fund administrator/trustees to double check that your scheme is fully compliant with current legislation. Luckily, if your pension fund is with Hanover on our latest SSAS Trust Deed & Rules then you will benefit from the full flexibility of the current legislation, brought in by the Taxation of Pensions Act 2014 (TOPA 2014). The details below are mainly aimed at plans offering full flexibility, so different rules could apply if you have alternative plans, such as contract based defined contribution or defined benefit schemes.

When a member passes away, the legislation allows trustees to use any remaining funds attributed to the member to pay death benefits from the scheme. These benefits can be split into two categories:-

- The trustees can pay a lump sum from the scheme.

- The trustees can pay a dependant/nominee/successor pension.

Benefits are paid at the discretion of the trustees, and therefore are usually paid outside of the member’s estate and free of Inheritance Tax (IHT). If the member passes away prior to age 75 then the above benefits can usually be paid tax-free. If the member passes away after the age of 75 then benefits are typically taxed as income in the hands of the recipient. Benefits may be tested against the members remaining Lifetime Allowance, depending on when they are paid and whether the member has drawn retirement benefits prior to passing away.

A tax efficient way of passing funds to the next generation

Although benefits are paid at the discretion of the trustees the member has the ability to state their wishes by completing an Expression of wish death benefit nomination form. With the ability to pay a lump sum and/or pension benefits directly from the scheme and the IHT benefits, members often use their pension benefits as a tax efficient way of passing funds down to the next generation. This can either happen on the death of the member or on the death of their spouse, if they elected a dependant’s pension when the member passed away.

Once death benefits are in payment, the trustees will liaise with beneficiaries to ensure that updated Expression of Wish death benefit nomination forms are completed. As long as sensible investment and pension drawing strategies are implemented the payment of death benefits can continue down several generations under the current legislation, so a member could potentially use their fund to provide benefits first to their spouse, then their children, then grandchildren etc.

A number of options available

There are a number of options open to members when considering death benefits; for example whether to pay benefits to beneficiaries directly from the pension fund, or whether to pay benefits to a family trust that then distributes payments to selected beneficiaries. This is where Hanover clients will benefit from being part of the wider Ince Gordon Dadds group. Our colleagues have a wealth of knowledge in family planning and providing IHT advice to individuals, encompassing not just the pension fund but also their wider income and estate planning. We would be happy to put you in contact with one of our partners who could provide you with specific expert advice based on your personal circumstances.

We hope that the above details are of use in giving some general guidance regarding the legislation surrounding the payment of death benefits. For further information specific to your particular circumstances please contact your usual Hanover consultant.

Articles published on this website were correct when they were written but may be out of date by the time you read them. While we make every effort to ensure that the information contained on this website is correct you should not rely on it without taking advice from a member of the firm.

By Richard Brazier | 7 March 2019

Many times I am asked by prospective clients why they should pay for ongoing advice on investment products. Surely, they reason, once the plan is set up my work as an adviser is completed and no longer necessary. So long as I have done my job well the fund will be invested in line with their agreed risk profile and will look after itself, in a contract that has been identified to meet their requirements.

Most of the people that I meet can absolutely see the benefits of the initial advice that we provide. They can see that we can help to identify their financial needs and quantify these into simple to understand objectives. From there we can recommend products that meet these objectives, and having agreed their attitude to investment risk, a portfolio to match this risk profile.

But why I am needed going forwards? Why should I pay you an ongoing fee once you have you recommended a contract and portfolio?

Of course, these are fair enough questions and I would liken it to how we look after our own cars. Once you have decided on the car you want and all the factors that come into this decision, most important being the colour of course, the garage’s job is done? Much as the same as ours is when you set up the recommended contract.

But is the garage’s job done at this stage? Much like an investment plan there are costs of running a car that can’t be avoided. With a car you will always have to pay for fuel and tax, and for an investment plan you will always have to pay for the annual contract charges and investment fund charges on a yearly basis.

You do, however, have the choice as to whether you pay for regular servicing on your car. If you elect to avoid this cost, the chances are your car will continue to work and get you from A to B. But you do run a greater risk of the car breaking down, especially over the longer term. Of course, just because you get your car serviced doesn’t guarantee it won’t break down but you are increasing the odds that it won’t.

And the same is true with paying for an adviser to regularly review your investment contract. This service means that you at least once a year get to speak to your adviser to review your plan. During which they can discuss whether your objectives have changed, whether your risk profile has changed and if your circumstances have changed to name a few. From there they can advise you if any changes should be made to your contract or investment portfolio. You will receive regular updates on how your investment is performing and you have access to your adviser throughout the year on an ad hoc basis.

Like the car, I can’t promise that by paying for an ongoing service will guarantee huge amounts of growth each year, much the same as a regular service doesn’t guarantee the car won’t breakdown. However, the ongoing service should provide reassurance that you have an adviser that is committed to looking after your investment contract. They will be able to ensure the investment continues to meet your needs and objectives as these inevitably change over the years.

July 2018

Insurance is a fundamental component in establishing and running a business. Most business owners are likely to take pains to ensure that they arrange insurance on their buildings, cars and equipment, and are covered for ‘loss of profits’ in the event of a catastrophe such as a fire or flood. Yet many businesses do not insure their greatest asset – the key people who ‘make the business happen’, for life cover. For relatively low costs, it is possible to help the business survive should the worse happen and one or more of the critical people become critically ill or die.

Who are your key people?

A key person within a company could be anybody who is regarded by the business as having a significant impact on the financial position of the company, and whose loss is likely to cause the businesses owners an urgent need to act swiftly to ensure continuity. This could be anyone whose role is “key” to the business because of their expertise, knowledge or contacts. They could also be crucial because of importance to the business; for example, if they own a significant amount of shares in the business. Also, business owners often lend money to their company, and these loans can be taken into account, as well as the servicing of ordinary bank borrowings such as overdrafts, and property loans.

Put simply, a key person assurance is a life or critical illness insurance policy on a ‘key’ person or persons within a business. In the event of death, serious illness or injury, the business can receive a fixed amount of money to buy the business some time to recover. The funds may be used to cover the cost of recruiting and training a new key person, providing temporary staff, or to compensate the business for lost revenue.

Further benefits

If a key person should die, banks are usually in a position to quickly vary the terms for short term borrowings such as overdrafts. With Key Person cover, the business can be in a position where it is able to inject a capital sum at a time of uncertainty, which would give considerable reassurance to creditors, helping the prospects for continuation into the future.

This valuable protection can be secured at relatively low costs.

How we can help

We are specialists in this field and can assist you with all aspects of the necessary arrangements. Contact Graham Smithson, Senior Consultant at Hanover Financial Management, to arrange an initial discussion, without obligation.