Author: admin

After entering the lockdown at the end of March, the overriding sense I get from most people is that they are now bored, and looking forward to a return to normal life. Thankfully, the lockdown measures are being eased, albeit at different rates throughout the UK. I was thankful that I was able to take the children over to see their grandparents for the first time in months a few days ago.

I have my fingers crossed that there won’t be a second wave, which will dent our own personal morale and no doubt the investment markets as well. Thankfully, as we have seen the lockdowns eased around the world a second wave doesn’t appear to have materialised at this time.

In fact, very heartening, the investment markets have continued to rebound from the low point seen in March, when the lockdowns were in force around the world. All the major indices saw positive returns through May, and this has been reflected in your investment portfolios. We are still a way away from the valuations seen at the beginning of February, but hopefully it is a source for optimism.

It never ceases to amaze me how the investment markets at times can seem oblivious to the economic data that is being seen, yet continue to produce positive returns. Of course, the reality is that they aren’t ignoring this data, more that this has already been priced into the markets. What adversely affects the global markets, in either direction, is surprising news. An example of this was seen recently when the expert consensus was that the US was going to see unemployment figures pushing 20%. The actual released figures actually showed that there had been a decline, which saw markets around the world increase on this news.

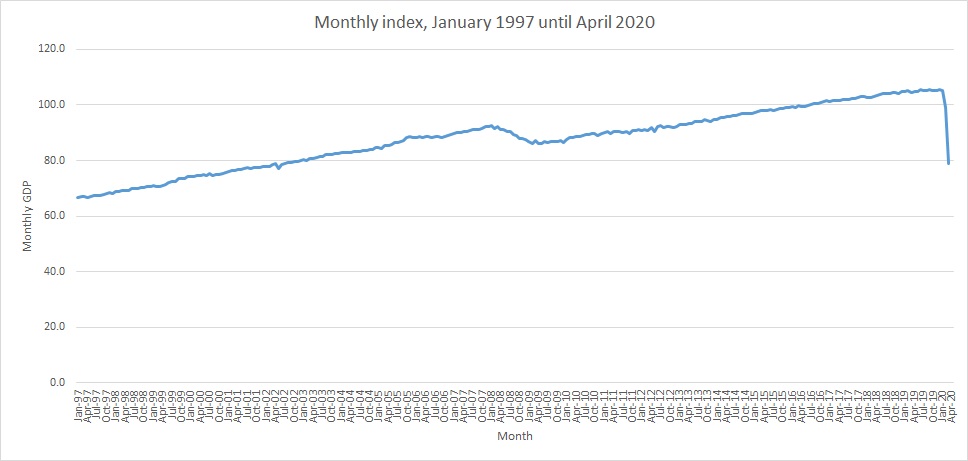

Having said all this, the economic figures that are being released, still take some comprehension as they show the effect this pandemic has had. For instance, the UK saw a drop of over 20% GDP in April.

Let’s hope that as the lockdown is lifted businesses can start to return to some degree of normal. Although I do think it will take some time and wonder what the ‘new normal’ will look like for all of us.

Although the global markets have been showing an upturn over the last two months, I still believe it is far too soon to say that we are over the worst. There is still a lot of volatility, and the true cost of this pandemic is yet to be seen. However, we will look to keep you as updated as we can on your investment portfolios during this time. As you know our view is that investment strategies should be for the long term, and that remains the case.

We are all available to speak to you, whether that is to discuss your investments or simply to catch up. Like you, we are all looking forward to being able to get out more, and to see you all in person.

Richard Brazier – Director – Hanover Financial Management Limited

|

|

I trust that you are all keeping well in these challenging times, and like me, are looking forward to a return to the ‘new normal’ soon.

I wanted to start this monthly update with some positive news; something that I think has been sorely lacking in the last few weeks. After the historic drop across the global financial markets from mid-February to the end of March, we saw an upturn from these same markets in April. One of my bug bears is that mainstream media only provide the negative news in relation to investment markets. Therefore, whilst news outlets were letting people know how badly the markets were performing during this period, they were much quieter during April when the markets began to improve.

Statistically speaking, the FTSE 100 fell to a low closing price of 4,993.89 on 23 March 2020, but by 30 April 2020 the closing price had risen to 5,901.21, and even passed 6,000.00 the day before. This meant the index had increased by over 18% in this time period.

Throughout the same period, the Dow Jones Industrial Average (a stock market index that measures the performance of 30 large companies listed on stock exchanges in the United States) increased by over 19%.

As a result, these increases were reflected, to a degree, in your own investment portfolios throughout April. Of course, as you will be aware, your portfolio will not be wholly invested in these stock markets, but depending on your risk profile, will have exposure to varying degrees in the global markets.

Despite the increases that were seen during last month, there was still far more volatility than normal. During the last few years, seeing a 2% increase or decrease within a day was a rare occurrence. However, over the last few weeks, this has been very common. The impact of Covid-19 is still causing financial uncertainty, and as a result, it is in my opinion still far too early to suggest the worst is behind us. However, the positive returns throughout April has to be welcomed with open arms.

Another area that is likely to cause more uncertainty in the performance of your investment portfolios will be the increasing tension between the US and China. Before the current crisis, there had been some easing of the tension between the two over their ongoing trade war. However, in the last week or so, the Trump administration have been more and more vocal in their claims as to where the Coronavirus originated; coupled with President Trump sending numerous anti-China tweets.

This, along with some negative economic news at the end of April, has seen some negative sentiment return to the markets. As this is an election year in the US, and I think it is safe to say that President Trump would have pinned a lot of his campaign on his success in creating jobs and market performance, he will be looking to blame China for this current crisis. If this conflict continues, I predict this will impact global market recoveries.

To finish on a positive note, I believe that finding a treatment and/or vaccine for the virus would probably outweigh the negatives of a second trade war between the US and China, at least in the short term.

We are still open for business, so if you have any queries or concerns at this time, get in touch with one of our financial advisers today.

Stay safe and we look forward to seeing you again soon.

|

Richard Brazier – Director – Hanover Financial Management Limited

|

|

As the global COVID-19 pandemic progresses, you may have queries and concerns about the performance of your investments. Specifically, our clients have seen a significant decrease in the value of their portfolios within a short space of time. We are here - to ask you not to panic, and to reassure you that during these difficult times, we are still open for business. For more information and advice, call one of our financial advisers today.

We recognise your questions and concerns - as we are all in the same boat. In my own experience, my lockdown has been very much bitter sweet to date. My son had a last minute dash back from university when he finally realised the government were locking down the country, and as mentioned in my previous blog article, my daughter was due to be sitting her GCSEs this summer, which of course, are now not going ahead. She has still been doing school work, whilst learning how her grades will be assessed in the summer.

It has however, been good to spend so much time with my family during this period - even if the shopping bill has somewhat increased!

On the bitter side, the lockdown has meant I haven’t been able to see my fiancée, who lives with her daughter in another town to myself. This has been incredibly difficult, although I am thankful for the wonders of modern technology which have enabled us to keep in contact via Facetime.

Of course, I realise that many people are having to deal with issues far more difficult than mine - and I am thankful that all my family and friends are all currently safe and well.

I have found this time to be quite reflective, a chance to assess all aspects of my life. For instance, I have been in touch with people close to me far more than I normally would have, and hope that this continues once the lockdown is over.

I, like many of our clients, have found that I have time to plan for my future; by making sure my Will, life cover and other financial aspects of my affairs are in place and up to date. If you need guidance whilst planning your financial affairs, we can place your individual concerns in the trustworthy hands of our legal experts at Ince.

Finally, during this enforced lockdown I have noticed that there seems to be some pressures to learn something new, like an instrument or a foreign language. In my opinion - do what it takes to get your through this period of time. If that is sitting in front of the TV, watching films or a new series on Netflix - so be it (no guesses for what I have been doing!).

|

Richard Brazier – Director – Hanover Financial Management Limited

|

|

Firstly and most importantly, I hope you are staying fit and healthy whilst managing to cope with the current circumstances and Government measures. These are certainly unprecedented times, and I can only keep my fingers crossed that life will return to normal soon.

In regards to investment portfolios, you will have no doubt seen how the global investment markets have fallen especially since the outbreak took hold in Italy, and subsequently the rest of Europe. Much of the fall was initially through fear and uncertainty, followed by concerns on how much damage this will do to the world’s economies in the longer term.

Governments and Central Banks have been very quick to announce a multitude of financial measures and stimuli but these have done little to alleviate the fears of the global markets. However, on the back of the latest stimulus plans that were agreed in the US, the markets rose for three days running at the end of last week. Showing how volatile the markets have been this hasn’t happened since February.

I would not like to say this will be the end of any falls, or that the bottom has been reached, as we are in unchartered territory. Indeed, already this week we have seen sharp increases and decreases in the markets and I suspect the volatility will continue for some time to come.

It is an easy thing to say, but I realise from my own investment portfolio not an easy thing to practice, which is not to panic at this time. History has always shown that shares have a good record of generating real returns over the long term, and these falls eventually become blips on performance graphs. It is also true to say that bear markets (where a market falls by 20%), such as the one we have now entered, have always been far shorter than bull markets (where a market is on the rise).

I realise this is a very unsettling period, as we all come to terms with the Government lockdown. I am having to get used to home schooling my daughter who was meant to be sitting her GCSE exams this summer! At Hanover we are all getting used to working remotely, as per the Government guidelines, which I do not envisage impacting on our service capabilities to you.

For more information and support, please do not hesitate to contact your adviser. In the meantime please stay safe and we look forward to seeing you soon.

Richard Brazier – Director – Hanover Financial Management Limited

To help employers through current difficult times, the Government has introduced the Coronavirus Job Retention Scheme. The aim is for employers to “Furlough” employees rather than lay off staff, with the Government paying some of the costs.

Coronavirus Job Retention Scheme

The main features of the Scheme are as follows:-

- In force for at least 3 months, starting 1 March 2020.

- Claim 80% of furloughed employee’s salary, up to £2,500 a month.

- Covers employers NI contributions and minimum Automatic Enrolment Contributions (i.e. 3% of salary above Lower Earnings Limit, which is £512 a month for March and £520 a month from 6 April 2020).

- The employee’s salary is subject to the normal deductions for tax, NI and Pension.

- For an employee on Statutory Sick Pay - they can be furloughed once this ends.

- An employee who is on Statutory Maternity Pay remains eligible for 90% of average weekly earnings for the first 6 weeks and lower of 90% of average weekly earnings or SMP at £148.68 per week up to 5 April 2020 and £151.20 from 6 April 2020. If employer offers enhanced pay during maternity, the additional payments are “wage costs” and are covered by the Scheme.

- The online system to claim will be available at the end of April 2020.

Pension Contributions

For furloughed employees the following applies:-

- Salaries under the scheme are pensionable so employees will need to pay pension contributions (unless they elect to opt out).

- If employer tops up the pay then the employee must pay pension contributions on the actual salary paid.

- Employers will receive support for employee contributions at the minimum AE required level, (with a band of excluded earnings) so if their scheme is more generous then they will need to pay the additional employer contributions.

- Employers still have all their obligations under both Automatic Enrolment legislation and their contractual commitments to staff (which they may seek to vary, but may need to take legal advice on the impact of this).

The Pensions Regulator (TPR)

The requirement to continue with Automatic Enrolment contributions has not been lifted, as some had hoped. However, the following should be noted:-

- TPR have indicated that they will give employers more time to pay their automatic enrolment contributions before using their enforcement powers.

- TPR are not suspending all enforcement activity, as employers still have a duty to pay pension contributions in a timely manner.

- Pension providers have been asked to be flexible when agreeing payment plans.

- In the longer term, all missed contributions must be made up in full, so that staff do not miss out.

Other Benefits

As a furloughed employee remains an employee on contract, all their normal benefits continue to apply. The precise details of how this works in practice are still being considered. However:-

- Group Life insurers have indicated that claims are likely to be paid based on pre furloughed salary.

- Group Income protection insurers have also indicated that claims are likely to be based on pre furloughed salary, but are considering the position as in some cases this could lead to the insured benefit being higher than the reduced furlough pay. With the issue of self-isolation they are also considering how the start of the deferred period should be determined.

- Group medical insurers have typically adjusted some of their benefits. For example, in some cases increasing the NHS cash benefit if admission is due to Covid 19, and funding video or telephone consultations with medical consultants. As the Government takes over much of the private hospital network and staff to assist in dealing with the crisis, private hospitals are starting to cancel non-emergency operations. For conditions already approved, typically if the procedure is cancelled, the approval can be carried forward. Physiotherapy sessions have largely moved online and insurers are seeing increased demand for video and telephone GP support and for online and telephone counselling services to assist with mental health and other issues.

- The coronavirus itself is not a critical illness covered by Group Critical Illness policies. However, if the virus leads onto a condition that is covered then insurers are considering claims.

- With schools and nurseries shut and many working from home, many employees are reducing their orders for Childcare vouchers. As this scheme is now closed to new entrants, employees should be reminded that if they take a break of more than 12 months then (under current rules) they will not be able to start again.

Comments

All of the above should provide some help to businesses in these difficult and challenging times. Claims under the Job Retention Scheme cannot be made until the portal is up and running which will not be until end of April. In the meantime, businesses are encouraged to apply for Coronavirus business interruption loans, from the British Business Bank, if they need funding support before it is possible to apply for the grants under the Job Retention Scheme.

All current employment legislation remains in place and as a reduction in salary is a contract variation, employers should generally seek the consent of employees to changes and seek legal advice to clarify the impacts and risks of any changes as necessary.

It is good to see that the Pensions Regulator is prepared to be flexible, but note that this is just on timing of the payments as ultimately all amounts due must be paid. The impact of investment return on member funds does not appear to have been considered currently, but if investment markets have risen significantly by the time payments are caught up there is a potential issue of claims for missed investment return.

It is important to remember that a furloughed employee remains an employee and entitled to all their normal employee benefits. As we move forward through this difficult time the position on how this will impact all benefits will hopefully become clearer, as insurers have time to consider the position but at the moment this is a fast moving landscape.

How we can help

If you would like to discuss any aspect of this article please don't hesitate to contact Robert Young or Graham Smithson.

July 2018

Insurance is a fundamental component in establishing and running a business. Most business owners are likely to take pains to ensure that they arrange insurance on their buildings, cars and equipment, and are covered for ‘loss of profits’ in the event of a catastrophe such as a fire or flood. Yet many businesses do not insure their greatest asset – the key people who ‘make the business happen’, for life cover. For relatively low costs, it is possible to help the business survive should the worse happen and one or more of the critical people become critically ill or die.

Who are your key people?

A key person within a company could be anybody who is regarded by the business as having a significant impact on the financial position of the company, and whose loss is likely to cause the businesses owners an urgent need to act swiftly to ensure continuity. This could be anyone whose role is “key” to the business because of their expertise, knowledge or contacts. They could also be crucial because of importance to the business; for example, if they own a significant amount of shares in the business. Also, business owners often lend money to their company, and these loans can be taken into account, as well as the servicing of ordinary bank borrowings such as overdrafts, and property loans.

Put simply, a key person assurance is a life or critical illness insurance policy on a ‘key’ person or persons within a business. In the event of death, serious illness or injury, the business can receive a fixed amount of money to buy the business some time to recover. The funds may be used to cover the cost of recruiting and training a new key person, providing temporary staff, or to compensate the business for lost revenue.

Further benefits

If a key person should die, banks are usually in a position to quickly vary the terms for short term borrowings such as overdrafts. With Key Person cover, the business can be in a position where it is able to inject a capital sum at a time of uncertainty, which would give considerable reassurance to creditors, helping the prospects for continuation into the future.

This valuable protection can be secured at relatively low costs.

How we can help

We are specialists in this field and can assist you with all aspects of the necessary arrangements. Contact Graham Smithson, Senior Consultant at Hanover Financial Management, to arrange an initial discussion, without obligation.

June 2018

Setting up a business is an exciting time, and while looking ahead at the opportunities that are opening up, perhaps the last thing on most entrepreneurs’ mind is the death or severely diminished health of either themselves or one of their business partners.

If you were to lose the contributions of a key business partner to ill health or worse, the impact on the workings of your business could be enormous. Not only would you lose the companionship of a business partner and possibly a friend, you would also lose their valuable expertise. Moreover, you could lose a share of your company to the spouses or beneficiaries of their estate, who may only be interested in the fiscal release-value of their inherited shares, and have little or no concern about the business’ future.

Steps to take

The answer is to think seriously about setting up some level of shareholder or partnership protection. This could help to safeguard you by enabling existing partners or company directors to purchase business shares from a deceased’s family if they should die or suffer a critical illness which prevents them from working. It is available to individuals in either a limited company, LLP or a partnership, and combined with good shareholder and ‘cross option’ agreements, can help to ensure continuity by providing insurance funds that you and surviving business partners could use to retain control of your firm should the worst happen.

Options

There are a number of ways to go about taking out these insurances. Each principal could take out a policy on each of the others; this is a popular approach when there are just two partners involved in a business. However, matters can become complicated when there are three or more partners involved.

There can also be inequitable situations if the age difference between the business partners is significant, because the cost of insurance for older persons will be much higher. For three or more partners therefore, it is a common approach for each business partner to establish a policy on their life and place it in trust for the benefit of either the company itself or in appropriate shares to the other business partners/directors. If the worst should happen, the remaining shareholders can then use the funds received from the insurance to fund the purchase of the deceased’s shares from their family or estate and redistribute them amongst the surviving business partners according to the Trust and ‘Cross Option’ Agreements.

Is it worth it?

The costs of protection can be relatively low for life cover only, and for business people, is as important as arranging their own personal Will and Lasting Power of Attorney. These issues are equally important for long established businesses where frequently we find that no regular reviews have been undertaken on the business protection arrangements and circumstances, particularly the value of the business, have changed.

How we can help

We can help you find the best option for you and your business and assist with all the arrangements, setup and management. In the first instance, contact Graham Smithson, Senior Consultant at Hanover Financial Management Limited.

Robert Young's article was published by Pay & Benefits in March 2016.

Family friendly benefits

Employers face many challenges and one is recruiting and retaining good quality staff to enable their business to thrive. Work-Life balance is perhaps an overused phrase but what can employers do to try and improve this and why should they?

The pressures of being a working parent are significant, so a key benefit for them is flexible working. There are many ways this can be achieved. Options include flexible start and finish times around core hours. The ability to work from home and time off to attend appointments during the day (provided that the time is made up).

A major event for any parent is the birth or adoption of a child. Children grow up incredibly quickly these days so spending time together particularly over the first few weeks are very important. Offering enhanced terms for maternity, paternity and adoption leave and the relatively new ability to share parental leave are all viewed as significant family friendly benefits by employees.

Childcare vouchers are a simple family friendly benefit to provided, generally by salary sacrifice. The cost of providing these will be mitigated by the savings in employer National Insurance contributions on the sacrificed salary. It should be noted that a new government scheme is being introduced in 2017 and there are winner and losers as a result of the changes so these need to be communicated.

One benefit that is popular and of benefit to all employees is the offer of retail and leisure discount vouchers or pre-paid cashback cards as they put money back into their pockets. They can help make treats such as meals out, trips to the cinema or theme parks more affordable and enable families to have some fun together. Many of these schemes give discounts at the high street chains we all use so that is money back on everyday spending. Employees that have a happy home life, come to work happy. This helps motivation and productivity while costing little to arrange.

On the issue of quality family time, the ability to buy additional holiday is another benefit many find attractive.

The ability to extend healthcare benefits such as private medical insurance and health cash plans is also attractive, even if the employer recovers the cost for the family members as this would be significantly cheaper than if employees sourced this themselves.

The overall message is that flexibility is key and so is good clear communication of all the benefits available. We are all time poor to some extent (working parents particularly so). Fortunately modern technology makes this achievable. Management must also buy into the benefits on offer and allow the flexible working to be achieved in practice. The provision of some of these benefits has a cost attached but employers should not underestimate the value that a happy, strongly motivated workforce has in terms of productivity, staff retention and staff recruitment.

Robert Young’s article in Pay & Benefits Magazine, published November 2016.

Should you Outsource Payroll and Employee Benefits Support?

Every employer needs payroll and many also decide to provide employee benefits. This means deciding whether to undertake this work internally, or utilising outside specialists.

Payroll

For any business ensuring that employees are paid on time, and correctly, is vital. Staff morale will soon suffer it this does not happen. If the business is to avoid fines it is important that information passed to HMRC is on time and accurate. With the introduction of Real Time Information (RTI) a few years ago, this can only be achieved electronically. HMRC has provided some basic tools but as the HMRC tool does not produce payslips this is of limited use in practice. There are many payroll systems on the market, some of which can be obtained at no cost, or low cost for very small businesses. Unfortunately payroll has its own language and whilst some aspects are straightforward, others can cause problems.

Why do it yourself?

For a small business owner who is prepared to invest some time and energy in investigating the market, choosing some appropriate software, learning how to use it, and who operates a simple pay structure, they may well decide that they can undertake this role themselves or add this to the role of their bookkeeper.

As the business and the size of the payroll grows, a payroll specialist may be employed, initially as part of the accounting team and eventually as a separate unit itself. The accuracy of payroll processing relies on the provision of accurate data, and as the business will need to produce this data, it may seem simpler to keep everything in house. The data can be reviewed, checked and processed without the need to consider how it can be exported safely and securely. Keeping everything in house may appear to provide greater flexibility to make adjustments more easily, respond to changes more quickly and keep everything within a small trusted team. You may prefer this feeling of having greater control of a task that is vital to keep staff happy and motivated.

Why outsource?

For some businesses, however, there is an issue in where this private data can be held securely and confidentially. They may operate from a small office or indeed no office at all. It may therefore be better for this data to be held securely at another place.

The amount of time involved should not be underestimated, particularly if payroll is run weekly with staff working variable hours.

As we move closer to the deadline for smaller businesses to deal with pensions Automatic Enrolment, this will add further complications and processes to the payroll function.

For a large business the outsourcing issue is different. Although they have the ability to hire the appropriate resources, there are times when they are under pressure to reduce headcount or fixed costs so may not wish to directly employ the resources necessary or fund the additional IT infrastructure that may be required, particularly when making payments to thousands of employees weekly.

A specialist outsourcer can bring a number of benefits and the real cost may be less than it first appears. As a business owner, you will have started your business because you have a passion for it, not due to a great desire to understand the world of payroll. If you devote the time you would spend dealing with payroll matters on your own business instead, then not only are you likely to enjoy this more but you will be concentrating on growing your own business with the rewards this will bring, leaving the specialist payroll bureau to deal with this essential administration, as this is their passion. If you employ staff to undertake the payroll function, they are likely to be salaried and therefore a further fixed cost overhead on the business.

An outsourcer will bring to you greater resources to deal with issues. If you only have one person who deals with payroll what happens if they are off sick at a key point in the pay cycle? A specialist outsourcer will provide in depth technical knowledge and have the experience and flexibility of a large team, yet you will only pay for the support you need.

In the world of payroll, like everything else, nothing stays still for long so there will be legislative changes to keep up with. A good software provider, if they have a good support function, should ensure that you are kept up to date on these issues but an outsourcer will alert to you to, and guide you through any changes, identifying the key issues that may impact your business. There are issues such as sick pay and maternity pay to deal with and the levels of these and the rules surrounding them do change from time to time.

It will not have escaped your notice that the UK has recently voted to leave the European Economic Community (EEC). No one is currently sure of the actual implications of Brexit, but this could lead to more changes. As each European country retained their own tax systems, it is to be hoped that there will not be too many implications for payroll processing. However an outsourcer will keep a keen eye on developments and be ready to react to any changes.

Employee Benefits

Many smaller businesses provide few employee benefits in order to keep the payroll processing as simple as possible. Others take the view that they pay their staff and it is up to them decide how to spend this money and whether to purchase benefits such as life cover or not. However, in a competitive world, it is often necessary for an employer to offer some benefits in order to attract and retain key employees needed to develop and grow your business. Some benefits are straightforward to provide but others are complex and again subject to their own language and legislative requirements.

If you are spending money on employee benefits, it is important that the benefits are obtained at the best possible price, constructed in the most appropriate way, and appropriate to the needs of your workforce.

While many very large companies employ benefit and reward managers, smaller businesses typically rely on either the Finance Director, Human Resources Director or business owner to deal with this.

Why do it yourself?

You would need to pay an outsourcer whereas an internet search and a few telephone calls will obtain at least a few providers of any benefit you may wish to offer. A little time in reviewing their offerings and a decision can be made and implemented. Indeed at the simplest level the provision of tea and coffee or in this healthy era, fresh fruit, may simply require for a small business the occasional trip to the supermarket. There are a number of other benefits that are relatively simple for a business to find directly such as childcare vouchers, or bike to work schemes. A good provider should also provide marketing materials and explain how the benefit impacts on payroll.

Other typical employee benefits such as pension, life cover, income protection, and private medical cover or health cash plans are not as straightforward.

Why outsource?

The time that it takes to undertake the required research should not be underestimated and may not result in finding the best provider.

If you have a small HR team, then their focus should be on the people issues, ensuring that you maintain a happy and motivated workforce rather than being involved in the detail of seeking the best providers for different benefits, particularly where they may have no experience in doing so.

An outsourced employee benefit specialist will give a smaller business access to the same skills that a large company may employ directly, with the ability to work with the appropriate in house personnel to formulate the appropriate benefit strategy for your business and then seek the best providers for each aspect.

At one level money purchase pensions are straightforward, but pensions has a language all of its own with much associated legislation and regulation. In addition the State provision of pension has changed recently and is likely to change again. It is not always easy to ascertain the full costs of an arrangement. Although the difference between an annual management charge of 0.4% and 0.6% does not sound much, your younger members of staff will be investing for 30 to 40 years and over this amount of time the impact of this can be significant. There is also the issue of where the funds should be invested which can have a significant impact on the final outcome.

Most large employers provide life cover but smaller employers have tended not to. However this is a popular benefit with staff and even for small groups can be purchased on terms that are far less than it would cost the employees direct. The key is knowing which insurers are competitive for smaller groups, which your outsourcer will know. Smaller business may decide not to offer benefits because they are too costly whereas a specialist could demonstrate that this is not the case and therefore enable a wider employee benefit package to be offered, perhaps helping attract staff to the business and retain them.

As we move into the post Brexit world, businesses will be faced with a number of changes particularly if they are trading internationally and new trading agreements are negotiated. The provision of State and private benefits has never been unified across the various countries within the EEC. As a result there are unlikely to be many changes directly as a result of Brexit. Of greater issue in the UK is the Treasury’s focus on salary sacrifice arrangement and the potential for this to be withdrawn. The provision of childcare is already changing in 2017 with the introduction of a new Government Scheme, but other benefits such as bike to work, provision of mobile phones, tablets and computers and optional employee pension contributions are tax efficient at least partially due to being provided on a salary sacrifice basis. This was considered in the last budget and no action was taken but a further review may take place.

In summary although there is a direct cost if a specialist outsourcer is used, and to some extent at least a perceived relinquishment of control, this can be offset by internal resources being more profitably directed to your own business, and savings being made due to the experience and knowledge of the specialist and the alternative proposals they can provide.

Summer Budget 2015

Earlier this month the Chancellor delivered the first conservative Budget for 18 years. Various announcements were made which affect UK registered pension schemes. A summary of the main changes is as follows:-

Tax relief on pension contributions for ‘high earners’

At present, the Annual Allowance for tax relievable pension contributions is £40,000 p.a.. Individuals also have the ability to carry forward unused allowances from the previous three tax years in certain circumstances.

The Chancellor announced that from 6 April 2016, anyone with an ‘income’ in excess of £150,000 will have their Annual Allowance reduced. This reduction will be tapered from £40,000 down to £10,000, with every £2 of income over £150,000 leading to a reduction in Annual Allowance of £1. Therefore, anyone with an income of £210,000 or above will have an Annual Allowance of £10,000. Furthermore, individuals will only be able to carry forward the tapered Annual Allowance to future tax years if this is unused.

The definition of income to be used is quite wide ranging and is expected to include salary, bonuses, rental income, salary sacrifice pension contributions, employer pension contributions etc. We will have to wait and see the makeup of the final legislation, but anyone with expected income within the above range will find it quite difficult to pinpoint the exact limit on their tax relievable contributions during the tax year in question.

Changes to Pension Input Periods (PIPs)

In light of the above proposals, the Chancellor has announced immediate changes to the Pension Input Period rules affecting all individuals. A PIP is the period over which a member’s contributions are valued in order to test them against the Annual Allowance. In most cases, a member’s PIP is aligned to the tax year, but this is not always the case. The changes that have been announced to the PIP rules are as follows:-

· Any PIPs active on 8 July 2015 will cease on that date.

· A new PIP commences on 9 July 2015 and will cease on 5 April 2016.

· Transitional rules will apply for contributions made on or prior to 8 July 2015, giving individuals an Annual Allowance of £80,000 (plus the usual carry forward rules).

· The Annual Allowance from 9 July 2015 to 5 April 2016 will be £0, but up to £40,000 of the unused Annual Allowance from the period up to 8 July 2015 can be added to this (plus the usual carry forward rules).

· Future PIP’s will be aligned to the tax years and individuals will no longer be able to alter their PIP.

All in all, these changes are quite complicated for the 2015/2016 tax year, but are simplified thereafter. Please contact your usual consultant if you or your scheme members need any assistance in working out the maximum allowable tax relievable contributions for the 2015/2016 tax year in light of the above changes.

Reduction in the Lifetime Allowance from 6 April 2016

As announced previously, the Lifetime Allowance will reduce from £1.25m to £1m from 6 April 2016. Protection will be offered for individuals who feel they will be affected by this reduction and we will be writing to clients separately on this issue as and when the protection regime is announced.

The Lifetime Allowance should increase in line with CPI from April 2018.

Changes to the taxation of lump sum death benefits

The benefits that can be paid on the death of a member altered from 6 April 2015. These changes were covered in previous newsletters. Any lump sums payable in respect of a member who passed away after the age of 75 are currently taxed at 45% for the 2015/2016 tax year. The Government previously indicated that from 6 April 2016 the tax rate would change to the recipient’s marginal rate and this change has now been confirmed. Any payments made to non-individuals (such as a company or a trust) will continue to be taxed at 45%. Lump sums payable in respect of members who pass away prior to age 75 continue to be paid tax-free, provided the payment is made within two years of the date of death and subject to the usual Lifetime Allowance rules.

Delay in changes to annuities in payment

The Chancellor previously announced that from April 2016 members who have already purchase an annuity will be able to sell these contracts on a secondary annuity market. This would presumably then allow the member to flexibly access the current capital value of the annuity. However, these plans have been put back to April 2017.

It should be noted that any decision to cash in an annuity contract (if the rules go ahead) should not be made lightly. It is likely that this secondary annuity market will be relatively small and it is doubtful that this will offer value for money to individuals.

Consultation on pension tax relief

Probably the most significant announcement in the Chancellors Budget was that of a Green Paper on the future of the pensions industry. The Government are asking if the current ‘exempt-exempt-taxed’ operation of the pension system is the best mode of operation. They are seeking opinion whether an alternative ‘taxed-exempt-exempt’ system would be clearer to understand and would be a greater incentive for savers.

The current system operates by tax relief being given on contributions paid into a registered pension scheme (exempt). The majority of the growth within the fund is tax-free (exempt). The benefits payable on retirement are taxed (taxed) except for the tax-free retirement lump sum.

The Government are asking if an alternative system might be better. Paying contributions from taxed income with no tax relief granted (taxed), growth within the fund tax-free (exempt), then benefits payable on retirement would also be paid tax-free (exempt). This is essentially the way the ISA regime operates.

The consultation ends on 30th September and anyone is free to respond to the consultation. It remains to be seen what changes (if any) will be made as a result of this consultation. We expect the Government are hoping that a move over to a similar system to ISA’s will attract more pension savings. However, overall it is likely that pension savers would lose out on a change of this nature, as the current tax relief granted on contributions would generally out-weigh the taxable benefits paid from pension funds under the current system. Furthermore, as the current system allows a tax-free lump sum to be paid, a certain portion of the current system operates on an exempt-exempt-exempt basis, and this would be lost altogether.

Please do not hesitate to contact your usual consultant at Hanover if you wish to discuss any of the above points in more depth.

This Update should not be relied upon or taken as an authoritative statement of the law. For more information, please contact us using the details shown.